6 things locum tenens physicians need to know about taxes

August 22, 2024

Locum tenens assignments provide a great deal of flexibility, the chance to experience new places, and a fun way to add diverse experiences to your medical career. It’s unique for all those reasons, and because it involves a different approach to taxes than typical W-2 employment.

Don’t let that scare you off. Sharon Gorman, vice president of tax for Global Medical Staffing, explains what you need to know about taxes as a locum tenens physician.

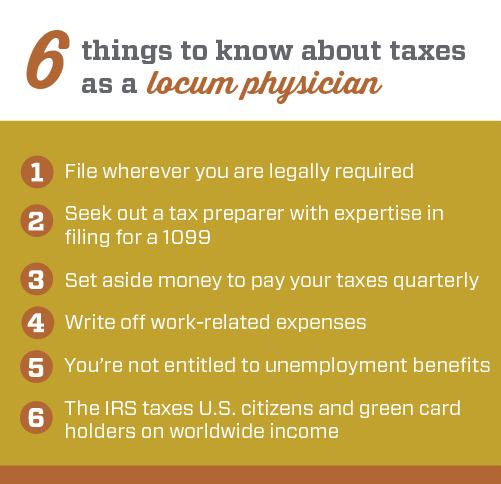

1. Make sure you’re filing wherever you are legally required.

Don’t assume you won’t have to file in both your U.S. state of residence and the place of your assignment. In most cases, you will need to do both.

2. Seek out a qualified tax preparer with expertise commensurate with your situation.

Because of the complexity of tax regulations, you should seek out a tax preparer with expertise and familiarity with your situation to ensure you’re filing everywhere you need to file. This person can also provide you with the best tax advice to minimize your tax liability within the law. For instance, if you’re a resident of Arizona doing locum tenens in California, work with a tax preparer with experience in both states and knowledge to apply tax regulations for a traveler like yourself. The tax preparer should be familiar with what constitutes residency versus traveler status for those two states, understand travel regulations and deductions, and know if other taxes come into play, such as gross receipts taxes or local income taxes.

Likewise, for a locum tenens assignment in New Zealand, work with a tax preparer experienced with taxes both in your U.S. state of residence and New Zealand.

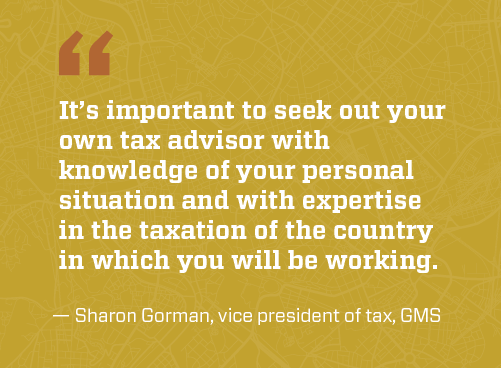

“It’s important to seek out your own tax advisor with knowledge of your personal situation and with expertise in the taxation of the country in which you will be working,” Gorman says. “Be aware when looking for a tax advisor, as the complexities of tax treaties require a specific knowledge base that most tax preparers don’t possess. Your tax advisor will need the expertise to consult both the tax regulations and treaties to determine the payment and filing requirements of each country.”

3. Set aside money to pay your taxes

As a locum tenens physician, you’re considered an independent contractor, so plan to set aside money to be able to pay your taxes quarterly. With the exception of California, which requires 7% withholding, no U.S. federal or state taxes will be withheld from your compensation. You will most likely need to remit federal and state estimated taxes each quarter, depending on your situation.

Want even more of your tax questions answered? Here's the ultimate guide to taxes as a 1099 (Locumstory)

4. Write off work-related expenses

Tax rates will be higher than for a typical W-2 position because, as an independent contractor, you pay not just the employee share, but also the employer's share of FICA taxes. However, independent contractors can write off work-related expenses, including, in some instances, travel and moving expenses. Consult your tax preparer early so you can plan accordingly and capture write-offs applicable to your situation.

Some good resources about deductions include: IRS Publication 463 Travel, Entertainment, Gifts, and Car Expenses; IRS Pub. 535 Business Expenses; IRS Pub. 334 Tax Guide for Small Businesses; and IRS Pub. 1542 Per Diem Rates (For Travel within the Continental United States).

5. You won’t be entitled to unemployment benefits based on work as an independent contractor.

In general, an individual cannot establish a valid unemployment claim based on earnings as an independent contractor. Unemployment compensation is a potential benefit that exists for individuals who have worked as employees and have lost their jobs through no fault of their own, and who are able and available for work as employees. A physician may file an unemployment claim if they previously worked as an employee. However, a staffing agency should not be listed as a previous employer on a claim, nor should any staffing agency compensation be reported as wages on that claim.

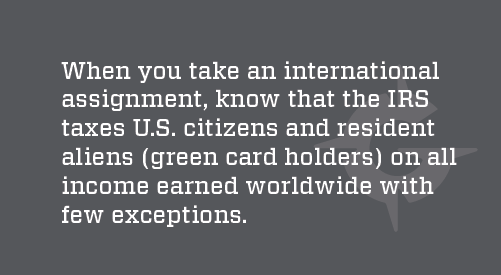

6. The IRS taxes U.S. citizens and green card holders on all income earned worldwide.

When you take an international assignment, know that the IRS taxes U.S. citizens and resident aliens (green card holders) on all income earned worldwide with few exceptions.

One exception to be aware of is the foreign-earned income exclusion. If you are a U.S. citizen or a resident alien of the U.S. and work abroad, you may qualify to exclude a portion of your income up to $120,000 for tax year 2023 (adjusted annually), for example. You can also exclude or deduct certain foreign housing amounts. A qualifying individual may claim the exclusion on earned self-employment income and reduce the individual’s regular income tax. However, the excluded amount does not reduce the income for purposes of the self-employment tax, and only a housing deduction is available. To claim the foreign earned income exclusion, you must be a bona fide resident of a foreign country or countries for an uninterrupted period that includes an entire tax year, reside in a tax-treaty country for an uninterrupted period that includes an entire tax year, or be physically present in a foreign country or countries for at least 330 full days during any period of 12 consecutive months.

Additionally, the U.S. has established tax treaties with several foreign countries–all with their own rules–to avoid double taxation. Under these treaties, residents or citizens of the U.S. are taxed at a reduced rate or receive an exemption from foreign taxes on certain items of income from sources within foreign countries. These treaties likewise establish rules so that residents of foreign countries pay taxes at a reduced rate or are exempt from U.S. taxes on certain items of income.

Educate yourself with these tax treaty basics ahead of consulting your tax preparer:

Additional tax considerations when working locum tenens internationally

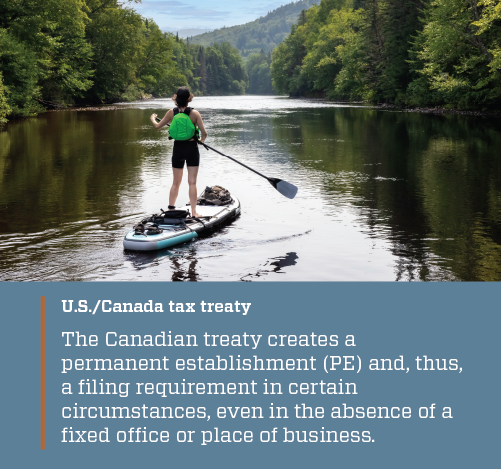

U.S./Canada tax treaty

As a general rule, anyone who provides services in Canada is subject to Canadian tax on the income earned from the performance of those services. The Canadian treaty creates a permanent establishment (PE), and thus a filing requirement, in certain circumstances, even in the absence of a fixed office or place of business. A provision in the U.S./Canada tax treaty would trigger an automatic PE in Canada if services were performed in Canada for 183 days or more.

According to the treaty, “A company or person will be deemed to have a PE in Canada if such person provides services in Canada for 183 days or more in a 12-month period and more than 50 percent of the gross active business revenue of the business is derived from services rendered in Canada.”

The treaty between Canada and the U.S. is complex. Sometimes income earned in Canada can be exempt from U.S. taxes—but a U.S. tax return must be filed. Be sure to consult a tax preparer with expertise in your situation.

U.S./New Zealand tax treaty

U.S. citizens working in New Zealand are generally exempt from New Zealand tax provided they are not present in New Zealand for more than 183 days in total in any 12-month period. Independent contractors that are present in New Zealand for more than 183 days are deemed to have a permanent establishment in New Zealand and are subject to a 30% withholding tax and will need to file an income tax return with New Zealand to recover any excess withholding.

Determining residency status in U.S. territories

If you earn income from American Samoa, Guam, The Commonwealth of the Northern Mariana Islands (CNMI), the U.S. Virgin Islands, or Puerto Rico, you may need to file a tax return with that possession, or you may need to file tax returns with the possession and with the IRS in addition to any resident state tax filings required.

An individual is generally considered a bona fide resident of a territory/possession if he or she (1) is physically present in the territory for 183 days during the taxable year, (2) does not have a tax home outside the territory during the tax year, and (3) does not have a closer connection to the U.S. or a foreign country. However, U.S. citizens and resident aliens are permitted certain exceptions to the 183-day rule. As with all cases, consult a tax preparer with expertise.

Although taxes can be complicated for locum tenens physicians, with the right guidance, you can make good tax decisions. Find out the number of days in the country/U.S. state that may trigger tax and filing obligations and consult an expert early.

Note: This information is intended to be general in nature and does not constitute tax advice. It cannot be used by any person as a basis for avoiding tax penalties that may be imposed by the IRS, any state or foreign government. Global Medical Staffing recommends consultation with a tax advisor to determine the tax implications for an individual provider specific to the individual and the travel assignment.